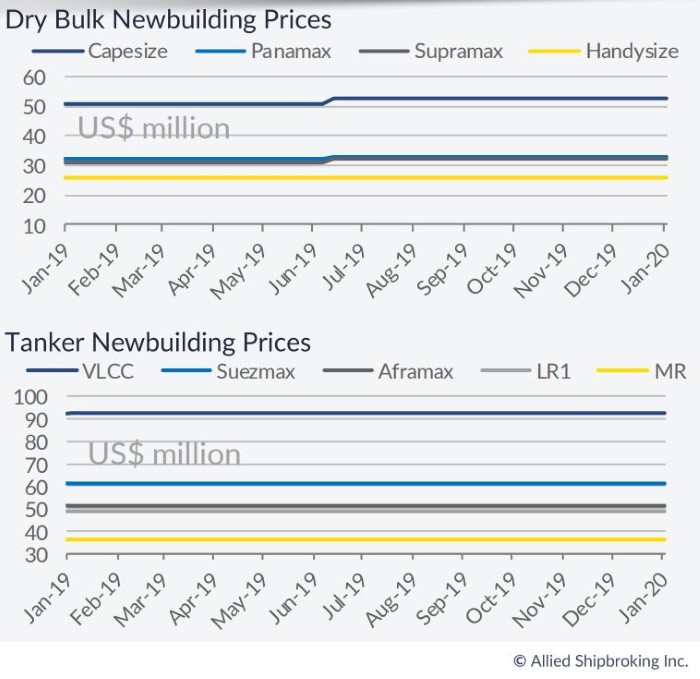

Ship owners have restrained their newbuilding and S&P investments in terms of new acquisitions since the start of the year, given the turbulent period that the freight market is experiencing. In its latest weekly report, shipbroker Allied Shipbroking noted that “the deteriorating freight market that has been noted from the beginning of year has shun a different light on the dry bulk market, keeping interest away from the newbuilding market. Given the current numbers, the expenditure of such an investment does not look to be justifiable right now. Last week we saw just two new orders surface, both from Chinese interests. This pattern is expected to continue over the following weeks, even if the freight market slump reverses, as current sentiment is still weak and running IRRs are very low, if not negative. As to the tankers market, things are much more positive, despite the last week noting a fair fall in freight rates. The robust sentiment is reflected in the steady stream of new ordering contracts that have emerged. Last week we witnessed 13 units being added to the orderbook. Interest from buyers is expected to remain intense over the following weeks, as this sector’s prospects remain positive for the time being”.

In a similar weekly note, shipbroker Banchero Costa added that “in the gas market, Hudong Zhonghua received an order from Petronas (Malaysia) at $ 240 mln for 2 x 80,000 cbm LNG carriers to be delivered during 2022. Japanese Owners N.Y.K. fixed a 170,00 cbm LNG carrier at Hyundai Samho to be delivered during first half of 2022 and the vessel will be employed on a long period TC to EDF. In the tanker business, Euronav signed a VLCC at Hyundai Samho at $ 94,2 mln to be delivered during first half of 2021. Always in Korea, Pan Ocean ordered at Hyundai Mipo 4 x MR tankers at $ 34 mln each with delivery between first half 2021 and 2022. In China, Torm signed 2 x LR2 scrubber fitted at GSI (Guangzhou Shipyard International) at $ 47,5 mln each with delivery during second half of 2021”.

Meanwhile, in the S&P market, the shipbroker said that “in dry segment the volume of sales was very modest: the most relevant was the sale of the Capesize ‘Aquacarrier’ 175,000 dwt built in 2011 at Jinhai which apparently went to Berge Bulk for region $18 mln. Price in line with the one-year younger sistership ‘Bulk Harvest’ which was sold in November for $ 19,5 mln. The wet segment recorded more sales than the dry sector: continued the good momentum for the VLCCs, the ‘Madison Orca’ 320,000 dwt built in 2010 at Hyundai HI was sold for region $50 mln to an unidentified buyer. The vessel originally built as VLOC is BWTS and scrubber fitted and the appetite for buyers seemed to be again for scrubber-fitted VLCCs since they can guarantee a daily premium of $20,000/d in freight compared to the non -fitted units. The VLCC ‘Katsuragisan’ 311,000 dwt built in 2005 at Kawasaki Sak’De was sold to undisclosed buyers for $35 mln. The price was $4,5 mln higher compared with the sale half a year ago of the similar unit ‘Aquarius wing’ 300,000 dwt built in 2005 at IHI. Active week also for the Suexmaxes with four sale registered: apparently an undisclosed Greek buyer purchased the sister-ships ‘Cape Bellavista’ and ‘Cape Baxley’ 159,000 dwt built in 2002-03 at Hyundai for $ 40 mln in total. We also understand that Adriatic Shipping apparently was the buyer of the Aframax Negishi Maru 106,000 dwt built in 2005 at Koyo Dock which was purchased for $17,8 mln”, Banchero Costa concluded.

Allied Shipbroking added that “on the dry bulk side, a further slow-down in SnP activity was witnessed last week, with interest from buyers having been limited following the recent slump in freight rates. Despite the deteriorating sentiment though, a few new deals were reported this past week, with focus given to the Panamax segment. This weaker appetite from buyers is expected to continue for a while, with any recovery being linked to either a freight market rebound or an increase in discounts being offered. On the tankers side, we witnessed a limited number of fresh deals as well this past week, despite the fact that prospects for this sector are still remaining healthy. It is likely that this lack of activity is just temporary, with the Chinese New Year possibly playing some small part, as interest remains strong amongst potential buyers. Given this, a fresh series of transactions is likely to transpire over the following weeks”, the shipbroker concluded.

Nikos Roussanoglou, Hellenic Shipping News Worldwide