Factoring financing relieves small and medium enterprises from the financial pressure by offering a chance to delay payments. It appeared long before venture capital, credits and equity investments, later lost its popularity for some time and then

resurrected by shifting to online.

At the current moment, factoring is tied up to flexible product offerings, improved turnover, optimum productivity, and increased profitability.

For example, factoring expansion data gathered in the EU clearly shows that factoring is growing significantly faster than the entire EU economy. According to the FCI report, in the past decade, the

annual eight-percent increase resulted in €1.7 trillion factoring turnover in 2018 and it keeps growing. Roughly 80% of the turnover is represented by the domestic factoring, which clearly dominates the market now.

Experts consider factoring a secured short-term financing tool, which reflects the real needs of the economy.

At the same time, one can suppose that factoring automation makes it easier and less time-consuming for all parties, and can substantially increase the volume of factoring contracts.

Despite the domination of stand-alone factoring fintechs, banks

don’t even think about giving up in the competition.

Digital factoring in banking becomes a powerful tool for banks as factors, helping to give their receivables finance business a brand-new look. Supply chain networks are working faster so automation is a matter of time. Great, if your bank is going to be

next.

Electronic factoring in banking: how can it look like?

The two primary tasks of factoring automation are to speed up the process and to cut costs. Moreover, centralized and more rationalized document storage can help “cut corners”: reduce paperwork and employee costs, increase the turnover and boost the bank’s

revenue, as a result.

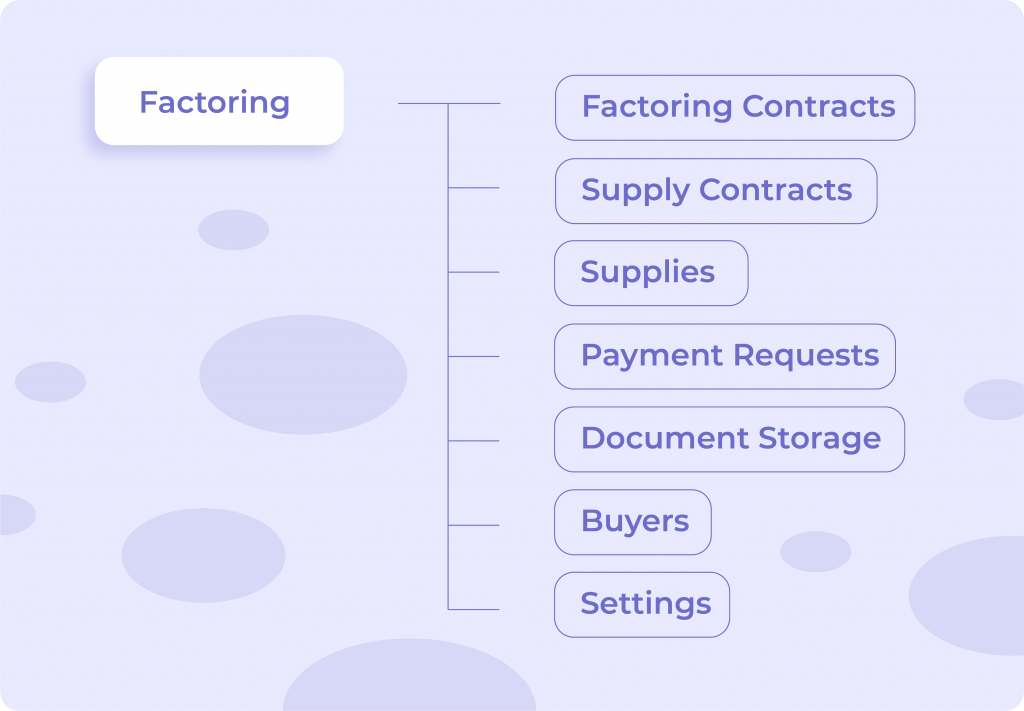

Factoring automation in banks implies:

- a single platform with a simple introduction of factoring services for your employees and customers;

- running transactions based on e-documentation verified by e-signatures;

- automated information gathering and automated registration of all the supply operations in whole;

- smart rights and restriction system, which grants different levels of access to some specified employees depending on their roles;

- customization to the needs of specific banks and customers;

- and more.

In the settings, it is possible to build custom scenarios and assign roles – so matching of payments and receivables can be done automatically.

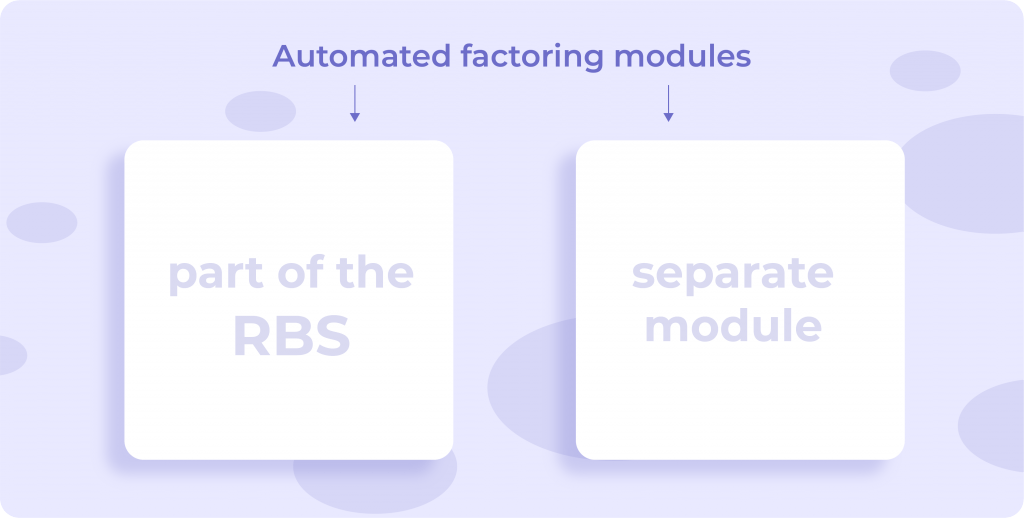

A factoring module in a bank: part of the system or a separate unit?

Automated modules are usually provided by a software vendor according to one of these options:

- as a part of an RBS (remote banking services) system

- as a stand-alone module.

For example, a bank had its digital channels and modules developed by the software company A. Later, the bank came up with a plan to have a factoring platform integrated into the existing system. It can be done the software vendor A again or by a software

vendor B or C.

However, based on experience, we consider the first option (adding a module right away) – an easier and a more rational idea along with the initial development of bank’s digital channels (for example, online or mobile banking for retail customers, separate

banking platforms for SMEs and so on).

Why? It’s as simple as that: the chance for fast and effective integration with the existing systems is higher. There is a ready digital infrastructure, user accounts, so the module is easy to adjust to integrate it with the rest of the banking service.

Just like with e-invoicing, it would be wrong to assume that e-factoring module can’t be installed on its own. Software vendors help to create internal accounts for bank employees and customers: logins, account tokens, the convenient access to the accounts

from any device. The developers can also provide initial training, if necessary. Also, the integration takes place: for example, uploading the existing banking data.

Automated factoring: Questions and Answers

Why all the channels and modules can’t be developed by the same software vendor?

Indeed, it would be logical to ask why one vendor can’t just install all the necessary modules and ensure their exceptional performance. Our own market research states that in 80-85% of cases of digital banking development banks select readymade software.

The providers of readymade digital banking solutions may have their own roadmaps, so either there can be no automated factoring solutions whatsoever, or the development of it can be planned for the future.

Therefore, the task of adding a factoring module to the out-of-box software providers may appear a sophisticated one.

Other reasons why banks don’t use the services of the latest vendor for having a factoring system installed are the following: financial issues, political situations or simply exhaustion from this very contractor.

Also, there can be issues associated with moving to the new infrastructure: when new top-notch solutions appear, there is no sense in investing in the existing ones. And again – it’s great when readymade software solutions include easy-to-add factoring modules.

If not – then a lot of questions come up.

Which advantages does a customized e-factoring module have?

There are independent fintech factoring companies that integrate with banks to provide factoring services. Such a partnership may seem cheaper and faster in the short-term perspective, but it limits the revenue.

Also, it has a lot in common with readymade banking software: any type of customization or expanding the functionality is close to impossible.

Own factoring software matches the specifics of banking activities and national regulations. Despite the fact that legal regulation of banking is similar in most countries, the structure of contracts, the insurance of non-payment risks and business conditions

of managing these risks greatly differ.

Banks can require different accounting data, types of statistics, and reports in various sections. All that derives from the business requirements of each bank. This is why many of them feel the basic functionality provided by third-party interbank platforms

or readymade modules is not enough.

A custom solution comes along with smooth integration and a ready API. Banks can also ask for a demo to try every integration step and analyze the way it works. Reliable vendors also provide full post-implementation support.

How would the flow look like?

Depending on the bank’s capabilities, such a system must be able to handle all the tasks associated with factoring: from applying for factoring services to effecting payments and keeping track of their status. The integration can be either dynamic, real-time

or in the offline mode, via data uploads – again, it all depends on the bank’s infrastructure.

Where are the contracts stored?

When it comes to supply contracts, it can be done either by the synchronization with the internal contract storage in a bank or by creating a separate factoring contract storage. The fact is that the customers must enter into a separate contract with banks

for factoring services. Such contracts additionally include clauses regarding insurance covering the risks of non-payment or delays in payment.

Based on our experience, some banks conсlude factoring contracts and keep them in other internal systems – in such cases, software vendors help download documents from the storage on ‘as necessary’ basis and help organize the business logic according to

it. Or all the older contracts are obtained from the storage, while all the new ones will be kept within the separate factoring module.

Summing it all up

By building a factoring system, you can simplify, automate and detangle complex processes being able to deliver a better customer experience, ensure compliance and reduce risks.

The level of customization and necessary features can be additionally discussed with the software development company. The points of discussion include:

- ensuring end-to-end document management;

- adding credit risk analysis functionalities

- implementing fraud detection systems

- having management features

- adding dashboards with statistics, and a lot more.